Note from Annabella Quiroga published in clarin.com day 11/09/2018 – HTTPS://www.clarin.com/economia/economia/argentina-dolariza-economia-ecuador_0_ryn-iLHdQ.html

Currency crisis

By what Argentina not dollarizes its economy as Ecuador??

Amid the depreciation of the peso, some analysts propose to adopt the scheme that governs the South American country since the 2000.

For most economists, dollarizing is not the solution.

It's a classic of Argentine history: every time the economy starts to get complicated mermaid songs appear sponsoring magical solutions. This time, with weight devaluing 100% so far this year and inflation moving to break the roof of the 40% annual, are heard again voices in favor of dollarization. However, analysts consulted by Clarín agreed that adopting the dólar as a national currency doesn't solve economic problems and leaves the country with fewer tools to get out of the crisis.

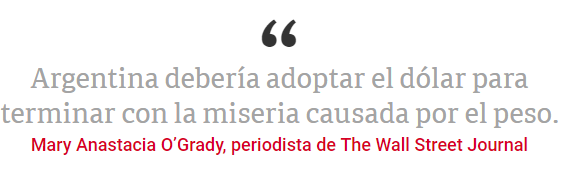

“Markets now predict that the economy will contract more than 2% this year and that inflation will reach 40%. The question that seems to be on everyone's mouth: why does it happen again, under a president who should represent change? The answer: because Argentina still has a central bank. To solve the problem once and for all, must convert it to dollars”, Highlighted.

For the analyst, Argentina lives above its means, with high taxes and regulations that make many activities un competitive. "The effect remains the same: inflationed debt and an economy with devaluations or defaults, or both", warned O'Grady.

Also the Argentine economist Guillermo Calvo, professor of the Columbia University which gained media relevance more than 20 years for having fore <1>ed the Tequila effect, opened a door in that direction. “Dollarization is something you have to think seriously about later because that can help us have a more reliable financial and monetary policy”, said last week in an interview for the newspaper The Nation. However, Calvo clarified that dollarizing “would not alleviate debt and current account deficit problems, y would take away an instrument, as is the exchange rate, that can help adjust”.

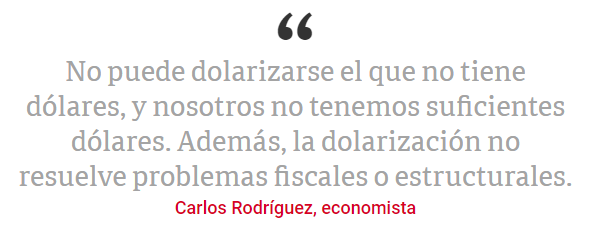

With the day-to-day life of the local economy on men, Argentine economists of different tendencies went out to reject the initiative. For Carlos Rodríguez - economist at CEMA and former Deputy Minister of Economics at the end of menemism, when convertibility still existed- dollarization is not an alternative. “I've said it countless times.: you can't dollarize the one that doesn't have dollars and we don't have enough dollars. Besides, dollarization doesn't solve structural problems on its own. Dollarizing is an alternative B to a weight collapse. For now that doesn't happen and there are no dollars. It would require huge refinancing of assets in pesos. In addition doesn't solve fiscal or structural problems. Ecuador is dollarized and has the same risk premium as Argentina”.

Ecuador adopted dollarization 18 years and kept it still during Rafael Correa's socialist tinge rule. Between 2006 y 2014, Andean country grew to an average of 4,3% annual, thanks to high oil prices and significant external financing flows. The expansion of the economy and social spending allowed reducing poverty in the 37,6% to the 22,5%. But in recent years the economy is deteriorating because of the low oil and the lack of new investment. Today Ecuador has no inflation, but the country's risk is higher than Argentina's: 757 basic points against 745.

Eduardo Blasco, from the consultant Maxinver, was one of the analysts convened almost 20 years by the then president of Ecuador, Abdullah Bucaram in the months leading up to dollarization. Bucaram wanted several Argentine consultants to explain how the experience of the 1 a 1 in Argentina. For Blasco, dollarizing Argentina's economy would be like trying to solve an alcohol problem by locking yourself in a cell. “It's an extremely debatable issue, when you adopt such alternatives gets his hands tied to make monetary policies. It's a simplistic and extreme measure that doesn't solve anything”.

In the case of Ecuador, that the 2000 had high inflation in dollars, dollarization worked at first. “But Ecuador remains with fiscal and economic problems and high country risk. It remains a country highly dependent on oil and other primary products and has a very low industrialization”, Blasco explained. Instead, it details that “Peru continued to maintain its currency and did much better than Ecuador, Just they took things seriously“.

Also Federico Furiase, from consultancy EcoGo, explained that “without fiscal discipline, with low reserve level, structural problems of competitiveness and inflationary inertia, dollarization just puts the problems under the carpet. After, the setting is more aggressive”. For the economist, “dollarizing the countercyclical role of monetary policy is lost. The only way to maintain a competitive real exchange rate for our exports without impairing the purchasing power of wages is to gradually lowering inflation, for which it is necessary to lower the fiscal deficit. And because dollarizing doesn't solve structural competitiveness problems, fiscal deficit and inflationary inertia and encourages dollarization of contracts along the way, the output is not only with more adjustment in real variables, such as production and employment, but withfinancial disruption“.

{kind=link}